9-Minute Read

Medical liability insurance in Florida is fundamentally a question of who controls a physician's capacity to practice medicine.

Understanding the nuances of Florida medical malpractice insurance in 2026 is vital to your practice.

The question of medical malpractice insurance in Florida has never been purely about risk transfer. It is, at its foundation, a question about who controls the physician’s capacity to practice medicine, and under what terms that control is exercised.

In 2026, the landscape has shifted in ways that demand clear thinking from the practicing physician, not as a passive consumer of insurance products, but as a professional who understands that every dollar spent on premiums is a dollar diverted from the direct care of patients

The Current State of Florida Malpractice Premiums

Florida remains among the most expensive states in the nation for medical malpractice coverage. Depending on specialty, a physician practicing in Miami-Dade County can expect annual premiums ranging from $40,000 for internal medicine to well over $200,000 for high-risk surgical specialties and obstetrics. These figures are not merely line items on a balance sheet. They represent the cost of practicing within a system that has, for decades, incentivized litigation over resolution and punished productive physicians for the systemic failures of institutions that were supposed to protect them.

The premium environment in 2026 reflects two competing pressures. On one side, the state’s tort reform measures, including the caps introduced under previous legislative sessions, have provided some degree of stabilization. On the other, the consolidation of the insurance market itself has reduced competitive pressure among carriers, allowing premiums to remain elevated even as claims frequency has, by most measures, declined.

A physician considering these numbers should ask a fundamental question: who benefits from this arrangement? The answer, when examined without sentimentality, points not to patients and not to physicians, but to the intermediary class of insurers, administrators, and legal professionals who extract value from the friction between doctor and patient. This is the same pattern we see repeated across the healthcare landscape, where third parties position themselves between the two parties with the most at stake and extract rents from the transaction.

The “Free Kill” Veto and What it Actually Means

The most consequential development in Florida’s malpractice landscape in recent memory was Governor DeSantis’s veto of the bill that would have repealed what critics call the “Free Kill” statute. This law, which limits wrongful death claims to cases involving surviving spouses or minor children, has been characterized by its opponents as a license for physician negligence. That characterization is not merely inaccurate. It is a deliberate inversion of the actual power dynamics at play.

The statute as it stands does not immunize physicians from accountability. Physicians remain subject to state licensing boards, federal regulatory agencies, hospital credentialing committees, peer review panels, and the full weight of professional ethical standards. What the statute does limit is the ability of the litigation industry to extract settlements from physicians through cases where the emotional valence of a claim outweighs its medical merit.

Consider the alternative that the repeal advocates proposed. Expanding wrongful death standing to adult children of any age would have created an enormous new class of potential plaintiffs. The practical effect would not have been improved patient safety. Safety is a function of training, systems design, and clinical judgment, none of which are enhanced by the threat of post-hoc litigation. The practical effect would have been a further transfer of wealth from practicing physicians to the legal-administrative complex, with a corresponding increase in defensive medicine, reduced access in underserved areas, and further consolidation of practice into large hospital systems that can absorb litigation costs.

As I wrote in “A License to Heal, Not to Kill,” the real danger to patients does not come from individual physicians practicing within the standard of care. It comes from the system-level decisions made by hospital administrators, health insurers, and pharmacy-benefit managers who dictate care from a distance. These are the entities that ration treatment, deny claims using automated algorithms, and cut staffing to protect margins. Yet the litigation apparatus, by design, targets the physician at the bedside rather than the boardroom decision-maker who created the conditions for harm.

The governor’s veto was, in this light, not a defense of physician immunity. It was a refusal to expand a system that already extracts enormous rents from the physician-patient relationship while doing nothing to address the structural causes of patient harm. True reform must include fundamental redesign of the vectors of accountability for poorly designed and implemented systems of care.

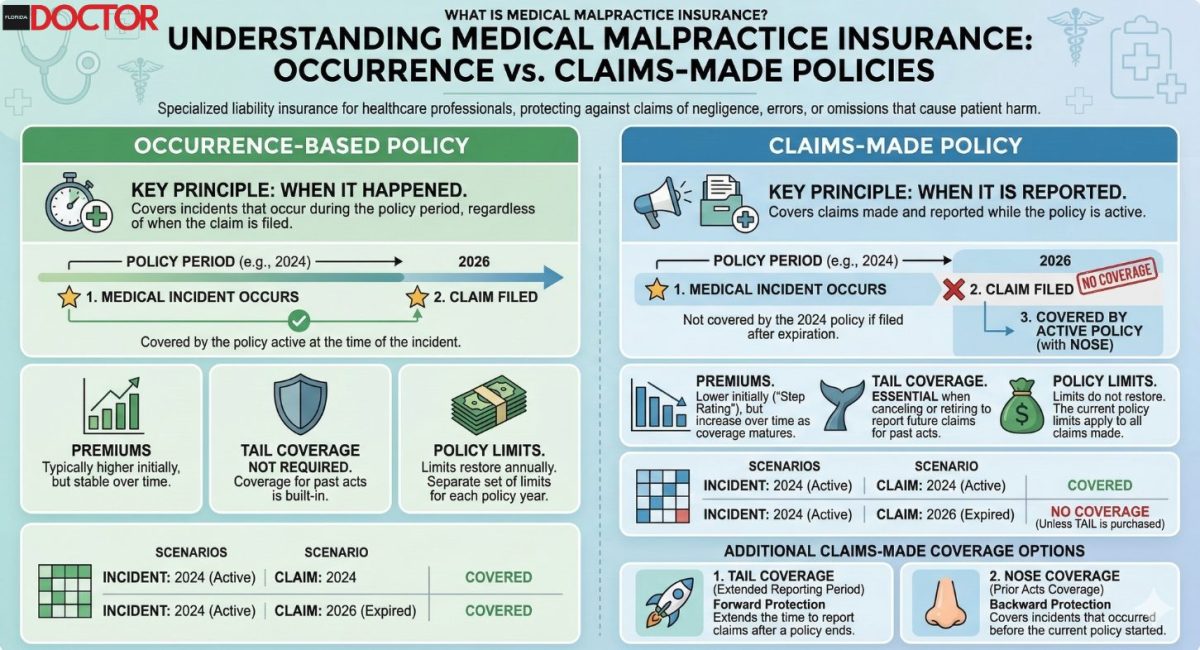

Understanding Your Policy: Occurrence vs. Claims-Made

For the practicing physician, the mechanics of malpractice insurance matter as much as the policy environment. The distinction between occurrence-based and claims-made policies is not a technicality. It is a structural decision that affects your financial exposure for years or decades after any given clinical encounter.

An occurrence-based policy covers any incident that occurs during the policy period, regardless of when a claim is filed. A claims-made policy covers claims filed during the policy period, regardless of when the incident occurred, subject to a retroactive date. The practical implication is that a physician who allows a claims-made policy to lapse without purchasing tail coverage is exposed to claims arising from past care with no coverage in place.

Tail coverage, often called an extended reporting endorsement, can cost between 150% and 250% of the final year’s premium. For a surgeon paying $180,000 annually, this represents a potential obligation of $270,000 to $450,000 at the moment of transition, whether that transition is retirement, relocation, or a change in employment.

The insurance industry has a clear preference for claims-made policies. They allow carriers to re-price risk annually and to externalize the cost of long-tail liability onto physicians through the tail coverage mechanism. This is not conspiracy. It is the predictable behavior of entities operating within a regulatory framework that permits such arrangements. The physician’s response should not be outrage but strategic clarity: Understand the terms, negotiate from a position of knowledge, and recognize that the policy structure itself is a product of regulatory capture, not genuine market competition.

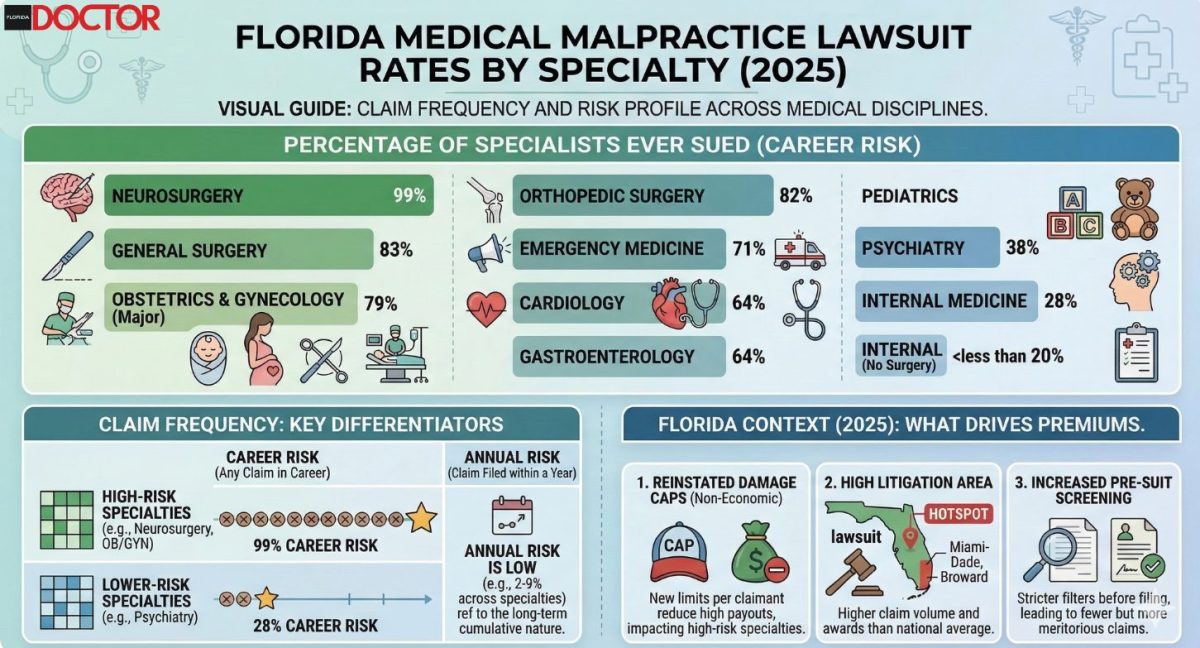

Specialty-Specific Considerations in Florida

The variation in malpractice exposure across specialties is not random. It reflects the interaction between clinical risk, litigation frequency, and the economic incentives embedded in Florida’s legal environment.

Neurology, my own specialty, occupies a middle tier in terms of premium cost but carries unique risks related to diagnostic uncertainty. Neurological conditions frequently involve progressive deterioration, long diagnostic timelines, and outcomes that are difficult to attribute to any single clinical decision. These characteristics make neurology cases attractive to plaintiff attorneys who can construct narratives of missed diagnosis or delayed treatment with the benefit of hindsight. Attempts by the clinician to be proactive can be intentionally misconstrued as overdiagnosis, and a skilled plaintiff may then play on the unsavory trope of the greedy doctor. This can leave even the most skilled practitioner feeling hamstrung and afraid to act in either direction, which translates to diminished access to care for the public.

Obstetrics remains the most expensive specialty to insure in Florida, with premiums reflecting both the severity of potential outcomes and the extended statute of limitations for birth-related injuries. Orthopedic surgery, general surgery, and emergency medicine follow in descending order, though local variation within Florida can be substantial. A physician practicing in the Panhandle will typically pay less than one practicing in South Florida, reflecting differences in litigation culture and jury composition rather than differences in clinical risk.

For physicians in any specialty, the strategic response is the same: Treat malpractice insurance not as a passive cost of doing business but as a risk management tool that should be actively managed, negotiated, and optimized.

The Self-Insurance Question and Market Alternatives

A growing number of Florida physicians, particularly those in independent practice, are exploring alternatives to traditional malpractice insurance. These include captive insurance companies, risk retention groups, and in some cases, practicing without traditional coverage entirely.

Florida law does not require physicians to carry malpractice insurance, provided they meet certain financial responsibility requirements, including posting a surety bond or letter of credit and providing notice to patients. This makes Florida one of the more permissive states for physicians who wish to self-insure or operate outside the traditional carrier model.

The case for self-insurance rests on a straightforward economic argument. If a physician’s actual risk of a paid claim is lower than the premium being charged, the difference represents a transfer of wealth to the insurance carrier. Over a career spanning 25 to 30 years, this difference can amount to millions of dollars that could have been invested, saved, or deployed in direct patient care.

The resolution of this tension is not ideological. It is actuarial. A physician considering self-insurance should obtain a detailed analysis of their specialty-specific, region-specific claims data, model the expected value of claims over their remaining career, and compare this to the cumulative cost of premiums. For many low-risk specialties, the numbers favor self-insurance or captive arrangements. For high-risk specialties, traditional coverage may remain the rational choice even at elevated premiums.

Captive insurance arrangements organized through physician-owned entities deserve particular attention. These structures allow physicians to provide coverage at cost while retaining investment income within the physician community rather than transferring it to commercial carriers. Several Florida physician groups have established successful captive programs in recent years. This is the kind of voluntary, market-based solution that emerges when physicians take ownership of the problem rather than waiting for legislative or regulatory solutions that invariably come with strings attached.

What a Genuine Market Would Look Like

It is worth considering what medical malpractice insurance would look like in a genuinely competitive market, one free from the regulatory distortions that characterize the current environment.

In such a market, insurers would compete on price, service, and claims handling. Physicians with strong safety records would pay meaningfully lower premiums than those with adverse histories. Policy terms would be standardized and transparent. And the overall cost of coverage would reflect actual claims experience rather than the inflated overhead of a regulatory compliance apparatus that serves the intermediary class.

Instead, what we observe in Florida is a market shaped by mandated coverage requirements for hospital privileges, carrier-friendly regulations that limit competition, and a tort system that generates enormous transaction costs relative to the compensation actually delivered to injured patients. Studies consistently show that less than 30 cents of every dollar spent in the malpractice system reaches patients. The remainder is consumed by legal fees, administrative costs, and insurance company overhead.

This is not a market failure. It is a regulatory failure. It is the predictable consequence of a system designed by and for intermediaries rather than the parties with the most at stake. When we talk about realigning resources in medicine, as I have advocated through the Medical Alignment Project, the malpractice insurance market is one of the clearest examples of malalignment between the interests of physicians, the interests of patients, and the interests of the intermediary class that profits from the friction between them.

Practical Steps for 2026

First, conduct a thorough review of your current coverage. Examine not only your premium and coverage limits but also the specific exclusions, the retroactive date on any claims-made policy, and the terms governing tail coverage.

Second, obtain competing quotes from at least three carriers. Use a broker who represents multiple carriers rather than a captive agent tied to a single insurer.

Third, evaluate your risk management practices with the same rigor you apply to clinical care. Documentation quality, informed consent procedures, communication practices, and clinical decision-making protocols all affect your risk profile. Carriers increasingly offer premium discounts for demonstrated risk management engagement.

Fourth, evaluate the structural alternatives. Captive insurance arrangements, risk retention groups, and self-insurance frameworks offer physicians the opportunity to take ownership of their risk management rather than outsourcing it to commercial carriers whose interests may not align with their own.

Fifth, engage with the policy process. The malpractice environment in Florida is a product of legislative choices made by representatives who respond to organized advocacy. The Atlas Accord exists in part to provide that organized advocacy, to ensure that physician voices are heard in the halls where these decisions are made.

Conclusion

Medical malpractice insurance in Florida is not a static cost to be passively absorbed. It is a dynamic variable shaped by legislation, litigation culture, market structure, and individual physician behavior. What defines the landscape is the aggregate of individual decisions made by tens of thousands of Florida physicians: Decisions about coverage, about risk management, about practice structure, and about political engagement. Each of these decisions either reinforces the existing system of intermediary extraction or moves incrementally toward a more rational arrangement, one in which the resources of the medical profession are directed toward their highest and most sacred purpose: The direct care of patients.

The choice, as always, belongs to the physician. And the time to exercise that choice with intention and strategic clarity is now.

Frequently Asked Questions

How much is medical malpractice insurance in Florida in 2026?

Florida medical malpractice insurance premiums in 2026 vary by specialty, with surgeons paying between 50,000 and 150,000 dollars annually, while primary care physicians typically pay between 15,000 and 40,000 dollars depending on location and claims history.

What factors affect Florida malpractice insurance rates?

Key factors include medical specialty, practice location, claims history, coverage limits, years of experience, whether the physician is employed or independent, and the insurance carrier chosen.

How can Florida physicians reduce malpractice insurance costs?

Physicians can reduce costs through risk management programs, maintaining clean claims records, choosing appropriate coverage limits, bundling policies, joining group practices, and completing insurer-approved continuing education courses.